The Indian cement industry is a vital part of the country’s infrastructure and economic progress. As the second-largest cement producer in the world, it plays a major role in contributing to India’s GDP, industrial production and employment generation.

With an installed capacity of around 700 Mn tons per year as of April 2024, the industry supports key sectors like housing, transportation and urban development. In FY23, the market size of the cement industry reached 445 Mn tons and is projected to grow to 625 Mn tons by 2029, with an expected CAGR of 7% from 2024 to 2029.

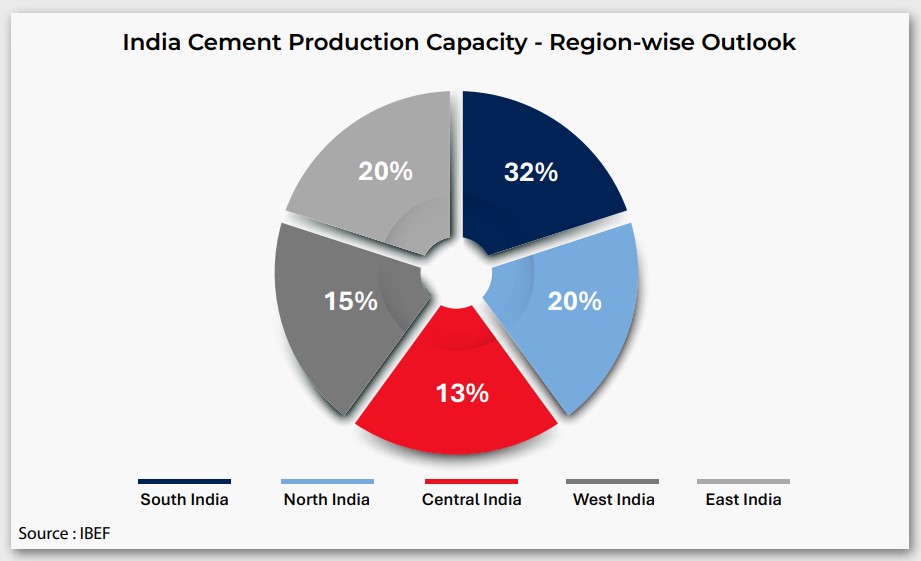

India’s rich and widespread limestone reserves offer strong growth potential for the sector. The country has 210 large cement plants, with 77 of them located in Andhra Pradesh, Rajasthan and Tamil Nadu. Region-wise, South India contributes about 32% of total cement production capacity, followed by North (20%), East (20%), West (15%) and Central India (13%).

Exports of panel cement, clinkers and asbestos cement products stood at INR 50.9 Bn in FY24, while imports were INR 14.4 Bn during the same period. Looking ahead, the industry expects an 8% increase in sales by 2025, supported by government investment in infrastructure, although it continues to face challenges such as lower sales realization in 2024.

The Indian cement industry is dominated by key players such as UltraTech Cement, Ambuja Cement, ACC, Shree Cement and Dalmia Bharat, together contributing over 60% of total production. Regional companies like Ramco Cements, JK Cement and The India Cements focus on specific local markets.

UltraTech Cement

Ambuja Cement

Shree Cement

JK Cements

Dalmia Bharat

Carbon Capture and Utilisation (CCU) Testbeds

The National Infrastructure Pipeline (NIP)

Bharatmala and Pradhan Mantri Awas Yojana (PMAY)

Strong Push for Sustainability and Green Tech

Capacity Expansion & Consolidation

Rise In Demand for Blended Cements

Robust and Growing Demand

Export Potential

Infrastructure Development