The Indian textile industry is one of the country’s oldest and most dynamic sectors, combining centuries-old traditions with modern manufacturing practices. It contributes nearly 2.3% to India’s GDP, 13% to industrial output and approximately 11% to total exports. This industry remains a vital pillar of the economy and is the second-largest source of employment after agriculture, directly engaging over 45 million individuals. The textile value chain in India is extensive, encompassing fiber cultivation, spinning, weaving, processing and garment manufacturing.

Moreover, the country is the world’s largest producer of cotton and jute, the second-largest producer of silk and a key supplier of man-made fibers. Strong raw material availability, skilled labour and diverse regional clusters such as cotton in Gujarat and Maharashtra, silk in Karnataka, wool in Punjab and man-made textiles in Surat give India a competitive edge.

Furthermore, the Indian textile industry also has a significant cultural dimension, with handlooms and handicrafts supporting millions of rural households while also contributing to exports. On the policy front, initiatives like the PLI Scheme, PM MITRA Textile Parks and incentives for technical textiles are strengthening infrastructure and attracting investment. With exports to over 150 countries, growing demand for technical textiles and rising emphasis on sustainability, India’s textile industry is well-positioned as a global hub for innovation, tradition & sustainable growth.

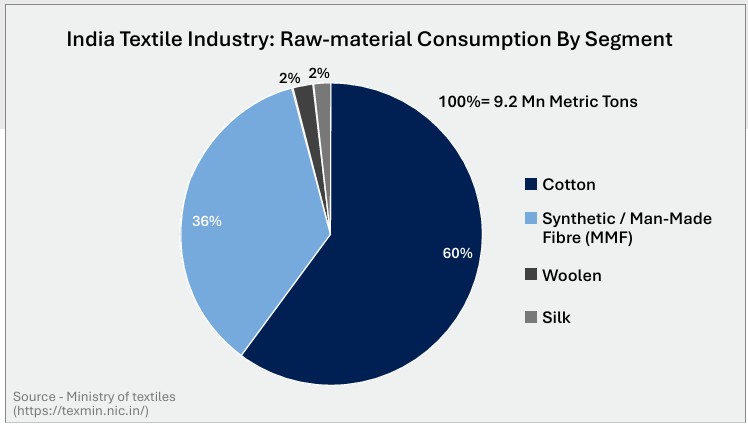

Cotton:

Cotton dominates India’s textile raw material consumption, accounting for approximately 60% of the total consumption basket. India holds the distinction of having the largest cotton acreage globally with 126.8 lakh hectares under cultivation, representing about 40% of the world’s cotton area. Cotton production supports approximately 6 million cotton farmers and 40-50 million people engaged in related activities. India cultivates all four commercial species of cotton and has a well-established Minimum Support Price (MSP) mechanism, operated through the Cotton Corporation of India Ltd. (CCI), to ensure remunerative prices for farmers.

Synthetic/Man-Made Fibre (MMF):

India is the second-largest producer of man-made fibres globally after China, with MMF textile and apparel exports valued at INR 712.5 billion in FY 2023-24. The government has established a Textile Advisory Group on MMF to deliberate and recommend on issues about the entire value chain of man-made fibres. To promote MMF production, the government has launched the Production Linked Incentive (PLI) Scheme with an outlay of INR 106.8 billion specifically targeting MMF apparel, MMF fabrics and technical textile products.

Woolen:

The wool sector is supported through the Integrated Wool Development Programme (IWDP), a Central Sector Scheme approved by the Standing Finance Committee with comprehensive objectives to position India as a competitive wool manufacturer. Moreover, the government provides marketing platforms and supports small woolen product manufacturers through exhibitions and trade promotion activities.

Silk:

India is the second-largest silk producer globally and the largest consumer, with production of 38,913 MT in 2023-24. The country has the unique distinction of producing all four commercial varieties of silk: Mulberry (accounting for 76.8% or 29,892 MT), Tasar (4.1% or 1,586 MT), Eri (18.5% or 7,183 MT) and Muga (0.6% or 252 MT). The silk industry is supported by the Central Silk Board (CSB), a statutory body established in 1948.

Production Linked Incentive (PLI) Scheme for Textiles

PM Mega Integrated Textile Regions and Apparel (PM MITRA) Parks

National Technical Textiles Mission (NTTM)

Samarth – Scheme for Capacity Building in Textile Sector

Sustainability and Green Textiles

Technical Textiles Growth and Innovation

Digital Transformation and Industry 4.0

Robust Ecosystem and Complete Value Chain

Comprehensive Government Policy Support

Large Skilled Workforce and Demographic Advantages

Growing Domestic Market and Consumption Base

Strategic Global Position and Export Competitiveness