India’s oil and gas sector is characterized by rising demand, high import dependency and systemic reforms aimed at achieving energy security and diversification. As the world’s fourth-largest refining hub, India is strategically expanding its capacity to 309.5 MMT per annum by 2028, balancing domestic needs with growing exports. The government is actively seeking to attract foreign investment through policies like 100% FDI in segments including natural gas, refineries and petroleum products, coupled with simplified exploration & production (E&P) rules, successfully reducing administrative hurdles.

Additionally, significant resources are being channelled into upstream exploration, with plans to increase the total exploration area to 1 million sq. kms by 2030, supported by new gas pricing reforms. Crucially, the sector is spearheading the energy transition through the National Green Hydrogen Mission and accelerating the 20% ethanol blending target to 2025-26, positioning the industry for a sustainable future.

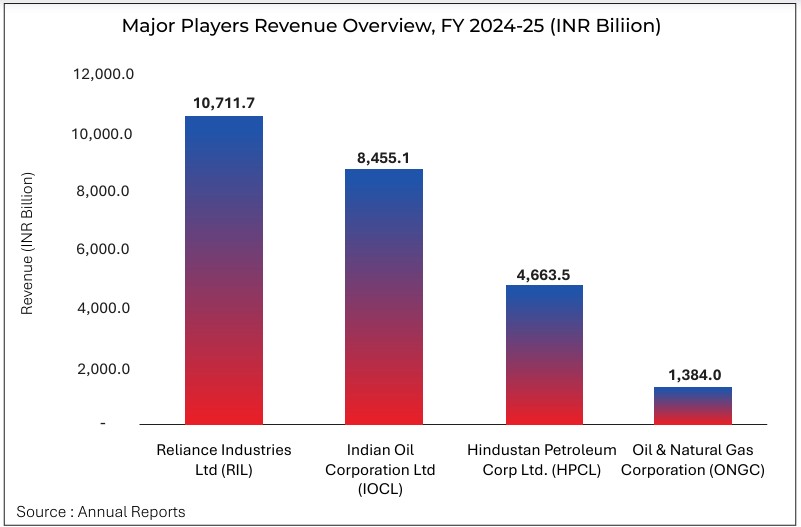

Reliance Industries Limited (RIL):

Indian Oil Corporation Ltd (IOCL):

Hindustan Petroleum Corporation Ltd (HPCL):

Oil & Natural Gas Corporation (ONGC):

Hydrocarbon Exploration and Licensing Policy (HELP)

Petroleum and Natural Gas Rules, 2025

Pradhan Mantri Ujjwala Yojana (PMUY)

Ethanol Blending Program (EBP)

National Green Hydrogen Mission (NGHM)

Increasing Shift Towards Gas-Based Economy

Digital Transformation and Advanced Technologies

Deployment of CCUS (Carbon Capture, Utilization & Storage)

Russia Crude Dynamics

Rapidly Growing Domestic Energy Demand

Strong Policy Support and Liberalised Investment Framework

Transition to Natural Gas & Biofuels Creates New Growth Avenues