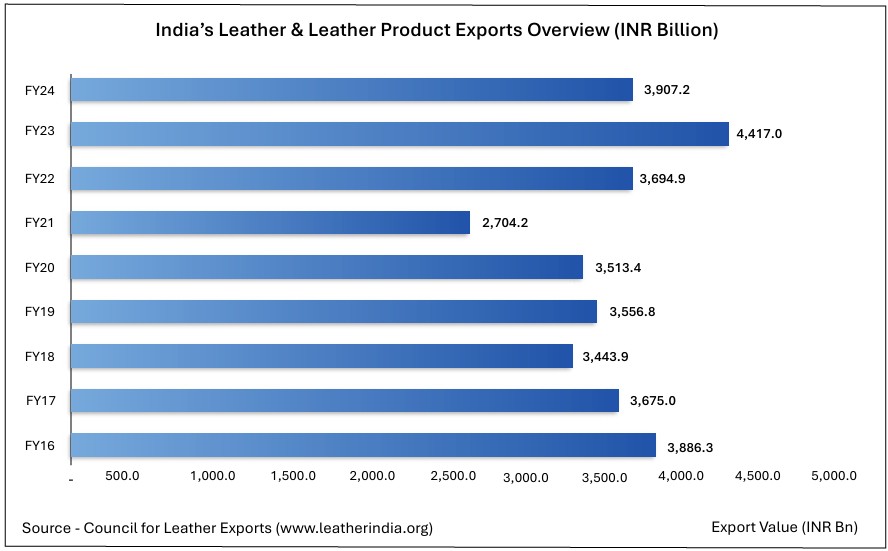

The Indian leather and footwear industry has shown resilience and recovery in recent years, supported by improving global demand and policy-led structural support. After the pandemic-induced slowdown, exports of leather and leather products increased from INR 2,704.2 billion in FY21 to INR 4,417 billion in FY23, before easing to INR 3,907.2 billion in FY24. This trend reflects recovery in key overseas markets such as the US and Europe, followed by normalization in global trade conditions.

Domestically, the industry is benefiting from strong consumption trends driven by urbanization, rising incomes and growing penetration of organized retail and e-commerce. India’s e-commerce sector, estimated at INR 10.8 trillion in 2024, is expected to reach INR 29.9 trillion by 2030, growing at a Compound Annual Growth Rate (CAGR) of 15%. Consumer preferences are steadily shifting toward branded, premium and lifestyle footwear, expanding demand across metro and non-metro markets. Digital platforms have further enhanced market access for manufacturers and brands, improving distribution efficiency and consumer reach.

Finished Leather

Leather Footwear

Footwear Components

Leather Goods

Leather Garments

Saddlery & Harness

No Leather Footwear

Indian Footwear and Leather Development Programme (IFLDP)

On March 3, 2022, the central government approved the Indian Footwear and Leather Development Programme (IFLDP), allocating INR 1,700 crore (INR 17 billion) for implementation up to March 31, 2026, or until further review, whichever comes earlier.

The seven sub-schemes under this programme include

Increasing Shift Towards Sustainability

Major Policy Support

High Availability of Raw Materials

Growing Market Value & Premiumization Trends

Robust Export Demand