India’s gems and Jewellery market is one of the most established and globally integrated sectors, driven by deep-rooted cultural significance, skilled craftsmanship and a strong export-oriented ecosystem. Cities such as Surat, Mumbai, Jaipur, Kolkata, Hyderabad and Thrissur act as key manufacturing and trading hubs, each specialising in distinct segments such as Surat in diamond cutting and polishing, Jaipur in coloured gemstones and Kerala in traditional gold Jewellery.

Market drivers include rising disposable incomes, urbanization and the premiumization of Jewellery consumption, particularly among younger consumers. The growing preference for branded and hallmarked Jewellery has improved consumer trust and accelerated the shift from unorganised to organised players such as Titan (Tanishq), Kalyan Jewellers, Malabar Gold & Diamonds and PC Jeweller.

Additionally, there is an increasing demand for lightweight and everyday Jewellery, especially among working professionals. Lab-grown diamonds are gaining traction due to affordability and sustainability appeal, with Indian players expanding capabilities in both manufacturing and retail. Growth in tier II and tier III cities, increasing women workforce participation and wedding-related consumption offer long-term domestic expansion potential.

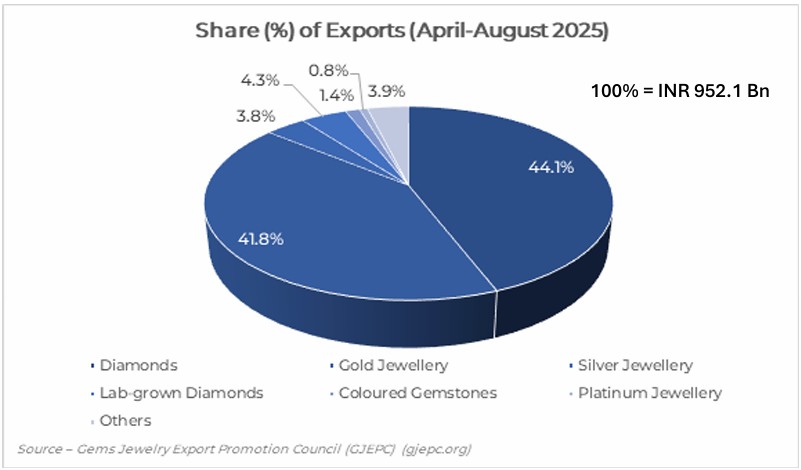

Diamonds

Gold Jewellery

Silver Jewellery

Lab-Grown Diamond

Coloured Gemstones

Platinum Jewellery

Supportive Budget Inclusion

Supportive Government Schemes

Global Promotional Events

Export Growth and Policy Support

Organized Retail Dominance

Global Market Dominance

Favourable Government Policies