Senior Advisor - Direct & International Tax

Buyback of shares implies a company repurchasing its shares from its shareholders. In a buyback issue, the company pays its shareholders a fixed value per share and re-absorbs that portion of its ownership that was previously distributed among public and private investors. The process enables the repurchase of shares from the existing shareholders usually at a higher price than the market price.

There could be several objectives as to why a company opts for buyback –

The Finance Act 2013 introduced the concept of taxing income distributed to the shareholders on buyback. In other words, income tax on capital gains on buyback of shares was introduced for the sake of transparency.

The Memorandum that explains the provisions of the Finance Bill 2013 is stated below::

“Unlisted companies, as a part of a tax avoidance scheme, are resorting to buyback of shares instead of payment of dividends to avoid tax payment by way of DDT, particularly where the capital gains on buyback of shares are either not chargeable to tax or taxable at a lower rate.

To curb such a practice, it is proposed to amend the Act, by insertion of a new Chapter XII-DA, to provide that the consideration paid by the company for the purchase of its unlisted shares is more than the sum received by the company at the time of issue of such shares (distributed income) will be charged to tax and the company would be liable to pay an additional income tax at 20% of the distributed income paid to the shareholder. The additional income tax payable by the company shall be the final tax on similar lines as dividend distribution tax. The income arising for the shareholders in respect of such buyback by the company would be exempt where the company is liable to pay additional income tax on the buyback of shares.”

Thus, with the aforesaid intent in mind, s. 115QA of the Income Tax Act 1961 was inserted which laid down the provisions relating to tax on income distributed to shareholders.

If the company fails to pay the additional tax within the due date prescribed under s. 115QA above, interest at the rate of 1% per month or part thereof shall be leviable for non-payment or short payment for the period beginning immediately after the last date on which tax was payable and ending with the date of the actual payment.

The Finance Act 2013 introduced s. 115QA of the Income Tax Act 1961. This section introduced the concept of tax on the shares repurchased and the same was applied to unlisted companies only. The Finance Bill 2019, amended s. 115QA to extend the applicability to listed companies as well.

Further, we also wish to draw attention to the fact that the income received by shareholders on income distribution is exempt in their hands under s. 10(34) of the Income Tax Act 1961.

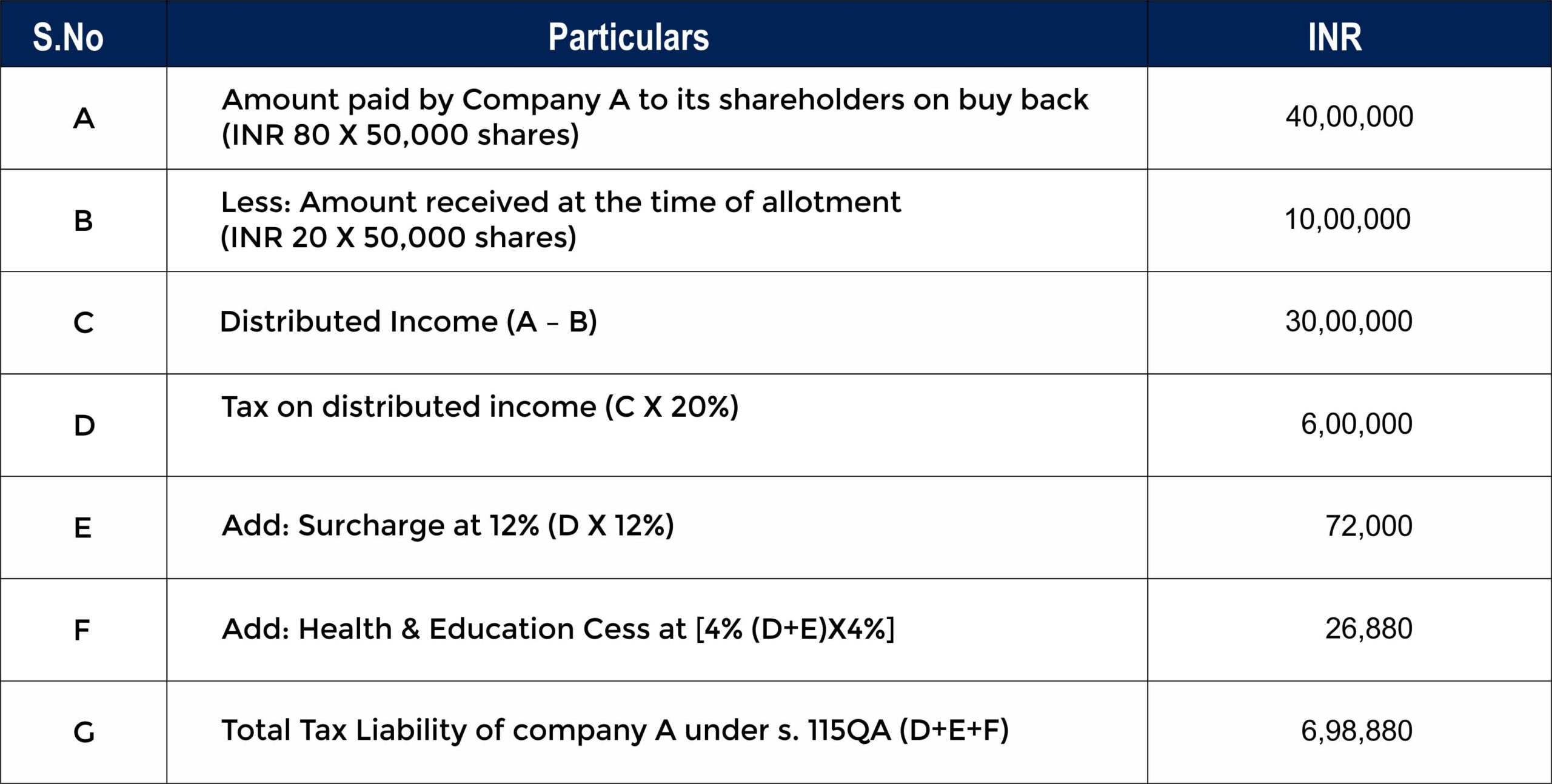

Company A decides to buy back 50,000 shares from its existing shareholders at INR 80 per share. Initially, the shares were issued to the shareholders at the rate of INR 20 per share. The calculation of additional tax under s. 115QA is given below:

Note: s. 115QA of the Income Tax Act 1961 is apply to both unlisted & listed companies. Hence, irrespective of whether Company A is a listed or unlisted company, Section 115QA would be applicable & tax on distributed income would be payable. Further, it is pertinent to note that irrespective of whether income tax under normal provisions is payable by the company or not, additional tax under s. 115QA shall be payable.

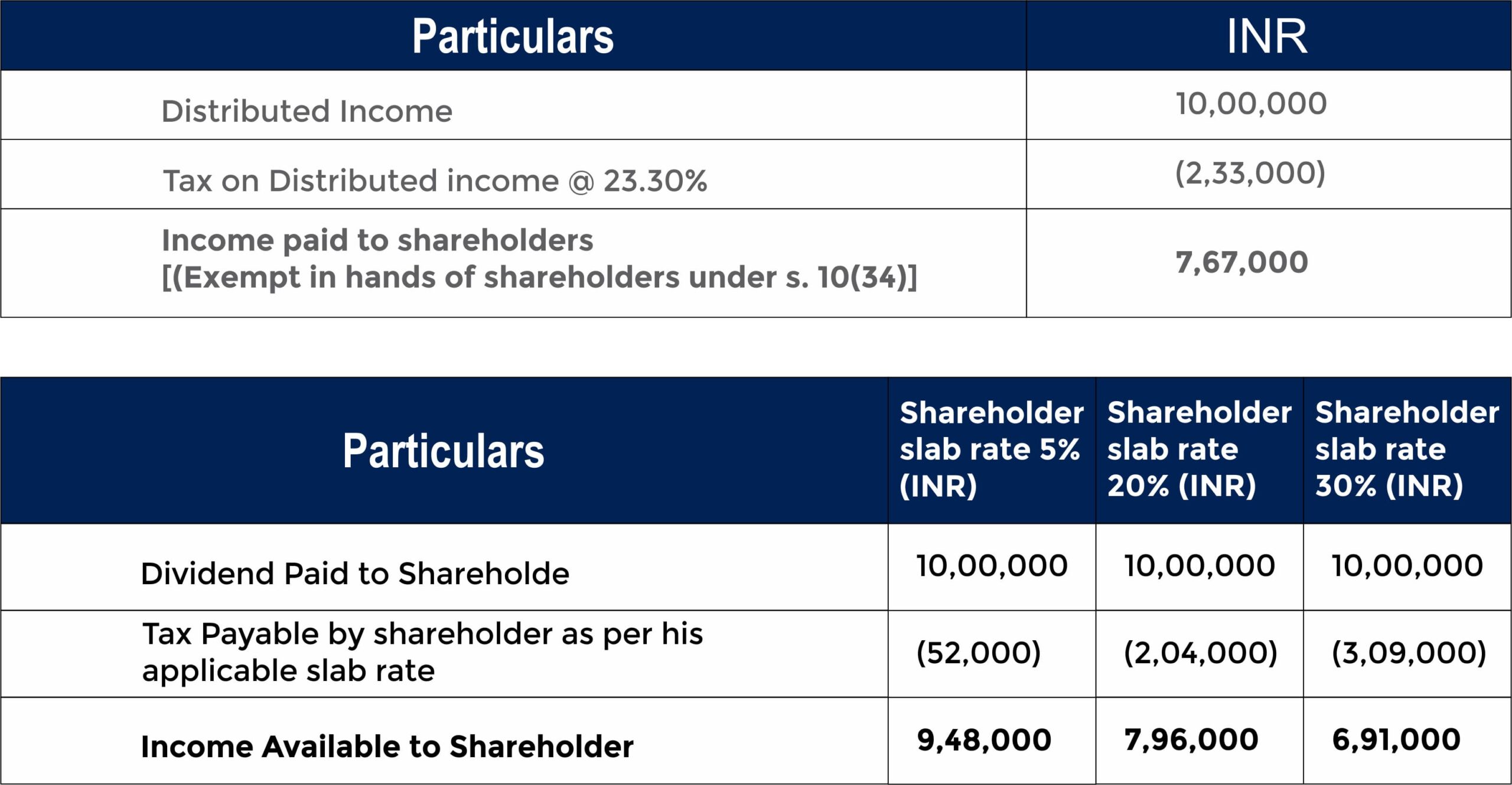

As per an amendment made by Budget 2020, DDT is no longer required to be paid by companies and such dividend is taxable in the hands of the shareholders at the applicable tax rates.

Buyback | Dividend Payout |

| A Company may purchase its own shares & other specified securities out of: | Dividend can be distributed by the company from |

| a. Its free reserves; | a. Out of the profits of the financial year under consideration; |

| b. The securities premium account; | b. Out of the profits of earned in the previous financial year or years; |

| c. The proceeds of the issue of any kind of shares or other specified securities.The maximum buy back is 25% or less of the aggregate of paid capital & free reserves of the company. Provided that in respect of the buyback of equity shares in any financial year, the reference to 25% in this clause shall be construed with respect to its total equity capital for that year. | c. Both of the above |

In the aforesaid scenario, it becomes evident that the dividend option is more beneficial to a resident shareholder who falls in the 5% and 20% slab rate. However, for an individual who falls within the 30% slab rate, buy back is more beneficial.