Senior Associate, Direct Tax

With this article, we would like to explicate the concept of Foreign Companies and PE in light of Indian Income Tax Act provisions.

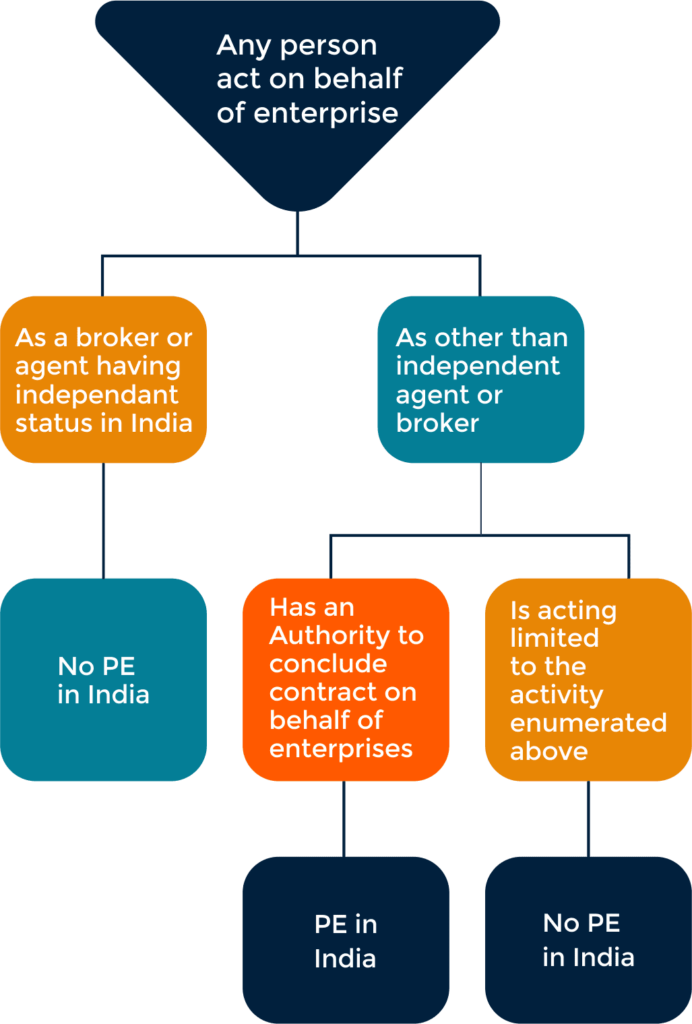

Let us understand the concept from the following graphical representation,

To conclude, we can say that a foreign company, non-resident in India may be taxed in India if it is operating through a Permanent Establishment in India.