Content Creator

The Goods and Service Act (GST) was a major tax reform introduced in India on 1st July 2017. The primary intention of introducing the GST was to replace many other state level taxes and to bring all taxes under a single umbrella. Before the introduction of GST, the complex Indian business and trade landscape suffered from tax evasion and also reluctance from Foreign companies to do business in India.

While the GST was also repelled by domestic establishments as every new reform, it helped to streamline the existing tax framework of India in a number of ways.

Through this article, we highlight the basic knowledge about GST which would answer some of the queries raised by businesses and individuals alike.

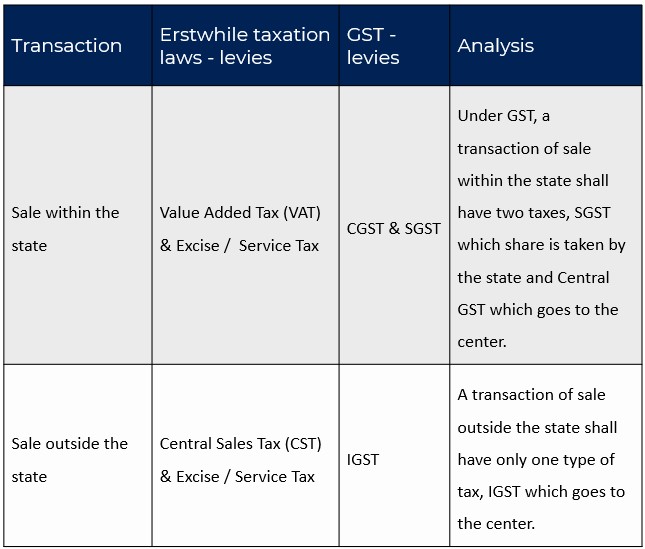

Since business entails a lot of inter and intra-state transactions and supply of goods and services it is imperative to know the different taxation laws applicable in various scenarios.

Intrastate transactions are subject to Central and State taxes. Interstate transactions are subject to Central Government i.e. IGST.

UTGST: Union Territory Goods and Service Tax is levied by the respective Union Territory for intrastate transactions of goods and services.

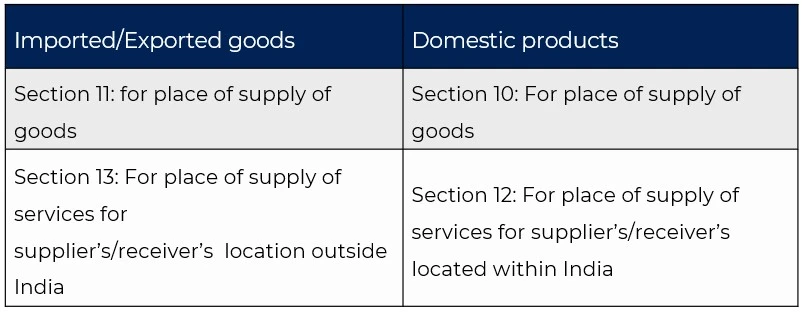

Since GST is a destination based tax, determining the destination of the supply of goods and services is indispensable.

An incorrect determination of the destination would cause levy of an incorrect GST.

To simplify this:

Under the ambit of GST Act, 2017, four sections govern the provisions for different transactions ultimately determining the taxable jurisdiction.

The time of supply plays an important role in determining the tax rate, value and due date. In order to mitigate tax evasion, the GST framework has given three provisions for determination of Time of supply of goods or services given below:

Time of Supply is the earlier of

It is noteworthy, that as per Rule 47 of CGST Act, the supplier of goods or services must issue an invoice within 30 days from the date of supply of goods/services. In case of the supplier being an insurer, banking company or a financial institution a provision of 45 days is given for issuing the invoice for the same.

Input Tax credit (ITC)was introduced to widen the scope of the Tax base and to mitigate double taxation suffered by any purchaser of goods/services during the life cycle of a transaction. Certain clauses govern the process of recovering the ITC as per the taxation framework.

Whether you are a supplier, agent, manufacturer or aggregator registered under the GST, you can claim ITC subject to the following:

“reverse charge” means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under certain conditions.

Notification No. 13/2017- Central Tax (Rate)

A GST Return document should be filed by a registered party and contains the below details:

Purchases

Sales

There are 13 types of GST returns: GSTR-1, GSTR-3B, GSTR-4, GSTR-5, GSTR-5A, GSTR-6, GSTR-7, GSTR-8, GSTR-9, GSTR-10, GSTR-11, CMP-08, and ITC-04.

GSTR-9C is an additional form to be filed by any registered person whose annual income is over 5 crore.

Minimum income for mandatory GST returns filing

The detailed GST framework is a radical step towards unification of the indirect taxes and to widen the tax base. The intelligent mechanism and clear-cut tax goal for India has effectively streamlined the indirect taxation landscape. Apart from mitigating tax evasion, it has encouraged FDI consistently in the past five years bolstering India to assume the next “manufacturing hub” position globally. In a robust world this is one positive step to increase India’s global presence exponentially.