India’s pharmaceutical market has established itself as a major global player, underpinned by its role as the world’s “pharmacy” and a robust manufacturing base. Key strengths include a vast portfolio of 60,000+ generic brands, extensive API production and strong compliance with international quality standards. India additionally supplies a significant share of global vaccines, contributing substantially to immunization efforts through UNICEF and WHO channels.

Strategic government policies, including Production-Linked Incentive (PLI) schemes, Foreign Direct Investment (FDI) facilitation and regulatory reforms, are further supporting sector growth. These measures aim to strengthen domestic API manufacturing, reduce import dependence and encourage higher-value segments such as biosimilars, specialty generics, and biologics. The Indian biosimilars market, valued at around INR 437 crore (INR 4.4 billion) as of May 2025, is projected to expand to approximately INR 1,649 crore (INR 16.5 billion) by 2034, growing at a CAGR of 14.2%.

Moreover, there is a growing emphasis on innovation, clinical trial capacity and regulatory cooperation to enhance global market access. With strong export growth, diversified product capabilities and continued investment, the Indian pharmaceutical sector is well poised for sustained expansion and enhanced global impact in both generics and emerging therapeutic areas.

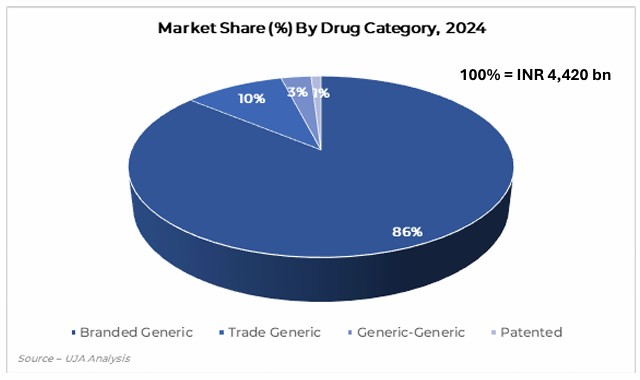

Branded Generic

Trade Generic

Generic-Generics

Patented Drugs

Production Linked Incentive (PLI) Scheme

Ayushman Bharat Digital Mission (ABDM)

Scheme for Promotion of Research and Innovation in Pharma MedTech Sector (PRIP)

The scheme is approved for a five-year duration, spanning FY 2023–24 to FY 2027–28.

Shift from “Make in India” to “Develop in India”

Integration of AI

Robust Export Demand

Liberal Foreign Direct Investment (FDI) Norms

Low Cost of Production